/Western%20Digital%20Corp_%20logo%20on%20sign-by%20360b%20via%20Shutterstock.jpg)

San Jose, California-based Western Digital Corporation (WDC) develops, manufactures, and sells data storage devices and solutions based on hard disk drive (HDD) technology. Valued at a market cap of $105.8 billion, the company is expected to announce its fiscal Q3 earnings for 2026 in the near future.

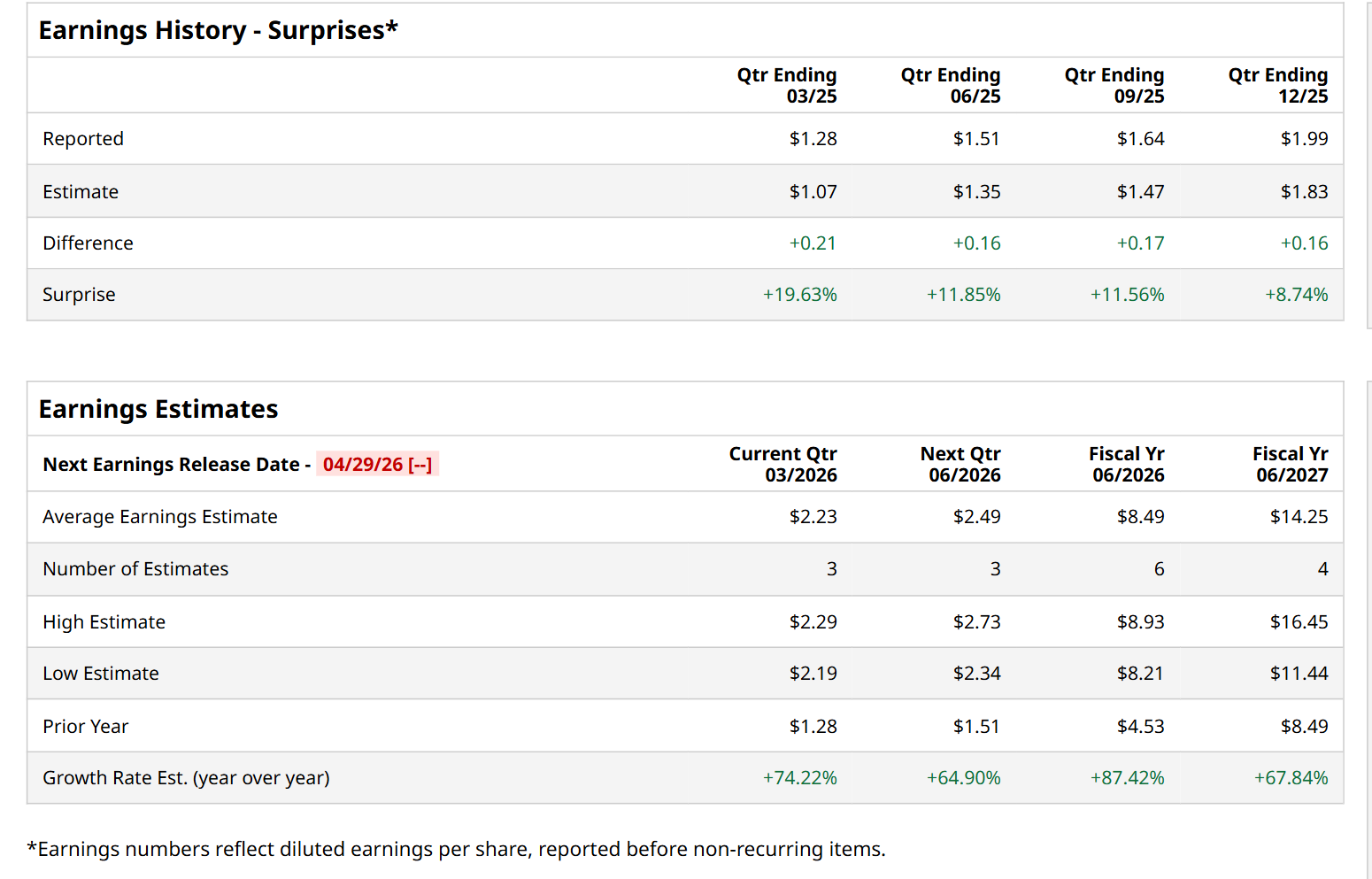

Before this event, analysts expect this tech company to report a profit of $2.23 per share, up 74.2% from $1.28 per share in the year-ago quarter. The company has topped Wall Street’s bottom-line estimates in each of the last four quarters. Its earnings of $1.99 per share in the previous quarter outpaced the forecasted figure by 8.7%.

For the current fiscal year, ending in June, analysts expect WDC to report a profit of $8.49 per share, representing an 87.4% increase from $4.53 per share in fiscal 2025. Furthermore, its EPS is expected to grow 67.8% year-over-year to $14.25 in fiscal 2027.

WDC has skyrocketed 960.4% over the past 52 weeks, significantly outperforming both the S&P 500 Index's ($SPX) 30.7% return and the State Street Technology Select Sector SPDR ETF’s (XLK) 49.8% uptick over the same time period.

On Apr. 6, WDC shares surged 3.1% after Morgan Stanley (MS) raised its price target on the stock to $380 from $368 while keeping its Overweight rating, citing robust demand for hard disk drives (HDDs).

Wall Street analysts are highly optimistic about WDC’s stock, with a "Strong Buy" rating overall. Among 25 analysts covering the stock, 20 recommend "Strong Buy," one advises a "Moderate Buy,” and four suggest "Hold." While the company is trading above its mean price target of $327, its Street-high price target of $440 suggests a 29.2% potential upside from the current levels.