/Wells%20Fargo%20%26%20Co_%20logo%20banner-by%20jetcityimage%20via%20iStock.jpg)

With a market cap of $234.6 billion, Wells Fargo & Company (WFC) is one of the largest financial services companies in the United States. The company provides a wide range of banking, investment, mortgage, and consumer and commercial finance products and services both domestically and internationally.

Companies valued at $200 billion or more are generally considered “mega-cap” stocks, and Wells Fargo fits this criterion perfectly. It operates through four main segments: Consumer Banking and Lending; Commercial Banking; Corporate and Investment Banking; and Wealth and Investment Management.

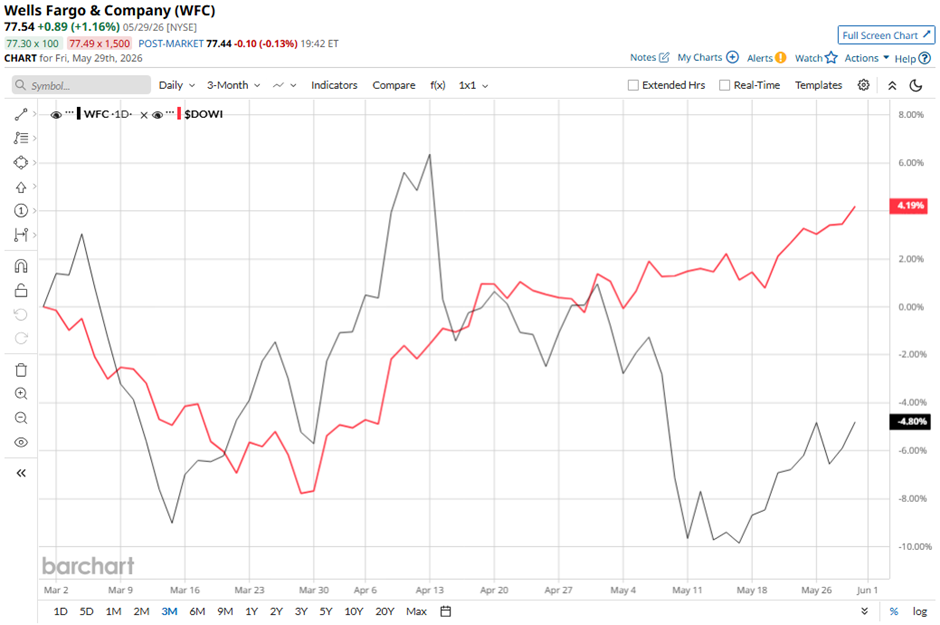

The San Francisco, California-based company stock has declined 20.7% from its 52-week high of $97.76. Shares of Wells Fargo have declined 4.8% over the past three months, lagging behind the Dow Jones Industrials Average's ($DOWI) 4.2% gain over the same time frame.

WFC stock is down 16.8% on a YTD basis, underperforming DOWI’s 6.2% return. In addition, shares of the biggest U.S. mortgage lender have risen 5.2% over the past 52 weeks, compared to Dow Jones' 21.2% increase over the same time frame.

The stock has been trading below its 50-day moving average since January. Also, it has fallen below its 200-day moving average since early February.

Shares of Wells Fargo fell 5.7% on Apr. 14 despite a slight EPS beat because investors focused on weaker-than-expected revenue and net interest income (NII). While Q1 2026 EPS of $1.60 exceeded estimates, revenue of $21.45 billion and NII came in at $12.10 billion, both missed consensus. Investor concerns were compounded by a 21.8% year-over-year increase in provision for credit losses to $1.14 billion, a decline in the CET1 capital ratio to 10.3%, and the company merely reaffirming its 2026 NII guidance of approximately $50 billion, below the consensus forecast.

Additionally, WFC stock has underperformed its rival, Citigroup Inc. (C). Citigroup stock has soared 7.9% on a YTD basis and 67.8% over the past 52 weeks.

Despite Wells Fargo’s underperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of “Moderate Buy” from 25 analysts' coverage, and the mean price target of $97.81 is a premium of 26.1% to current levels.